This month the Connecticut Chapter of the National Association of Social Workers (NASW/CT) issued results of a survey as to interactions between licensed clinical social workers (LCSW) in private practice and health insurers.

The insurance survey report is consistent with a previous report by NASW/CT that shows continuing and persistent barriers put up by health insurers that is driving private practitioners to limit or drop health insurers, thus reducing access to mental health care.

The report had responses from 398 members of NASW/CT all in clinical private practice. Information sought included whether the respondent participated in commercial and/or public insurance, if they did participate do they limit the insurers they accepted, what concerns and problems they faced dealing with insurers and if they were considering no longer participating with insurance plans within the next 12 months.

The findings of the survey indicated that significant problems with insurers, all long-standing, are indeed causing LCSWs in private practice to leave health insurance panels. When asked if the LCSW accept commercial insurance 27% reported they do not. When asked about public insurance (Medicaid, Medicare, etc.) the percentage rose to over 33%. Of even greater concern, a whopping 57% limit the insurers they will accept. When asked if consideration was being given to completely divorcing from insurance panels within the next 12 months, a most troublesome 41% answered in the affirmative. A year from now, if only a quarter of those considering leaving insurance panels join those no longer taking insurance that would mean close to half the LCSWs in private practice would no longer accept consumers who need to use their insurance coverage for mental health treatment. Licensed social workers deliver approximately two-thirds of all mental health services in Connecticut. From conversations of representatives of the other behavioral health professions , our survey findings are consistent with their members experience, meaning Connecticut is rapidly facing a behavioral health access crisis driven by the health insurance industry.

So, what are the factors that are driving behavioral health providers to no longer accept insurance or limit the insurers they will accept?

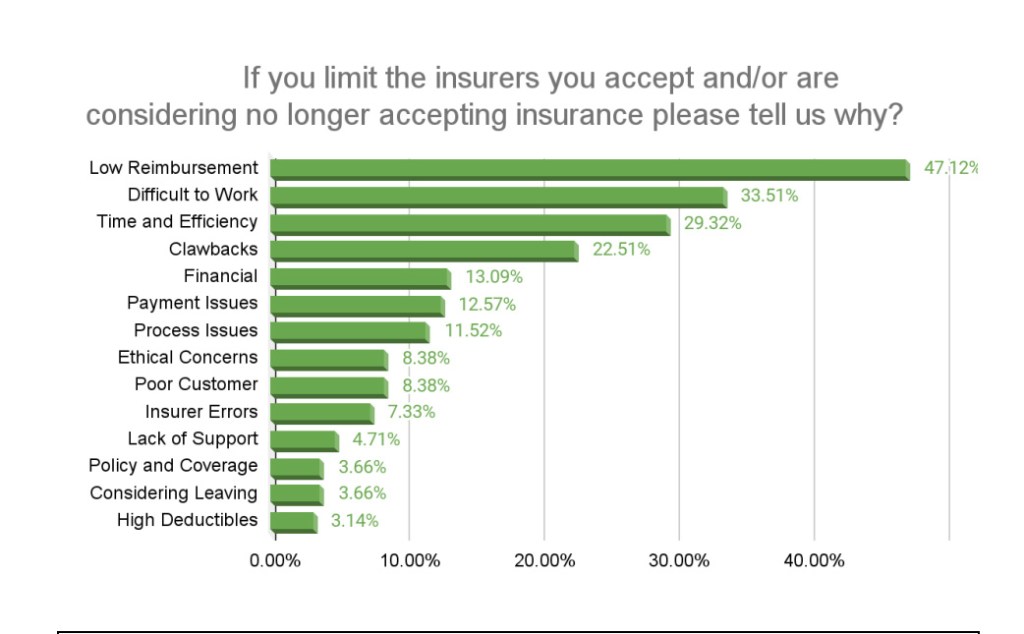

The number one problem is low reimbursement rates. This issue was reported by over 47% of survey respondents who limit or are considering no longer taking insurance. Many providers have not had an increase in their reimbursement for years and even those who have report the amount to be insufficient. From a business perspective it is a bad business decision to be an insurance provider when costs of practicing are rising but not reimbursements. Most LCSWs who accept insurance could increase their annual income by up to 50% if they only saw private pay clients. The social work profession is committed to serving all income groups but it gets harder each year to continue to do so. The financial hardships of being on insurance panels can no longer be minimized or ignored.

Administrative hassles with insurers were listed as the second biggest concern with nearly 34% of respondents citing this issue. Along the same lines over 29% noted the long wait times on the phone and needing to make multiple calls to resolve problems with claims as a frustrating problem. Many of these respondents pointed out that the time spent arguing with insurers takes away from time better used seeing additional clients. Similarly, payment issues such as delayed payments and claim processing errors was frequently mentioned as problematic.

Retroactive denial of previously authorized treatment (claw backs) was mentioned by over 22% of respondents. Of the 33 states that regulate the length of time an insurer can go back and retract payments 31 states have limits between six to 24 months. Connecticut has the longest look back period of 60 months. Insurers seek predictable business conditions yet they cause a complete lack of financial predictability for behavioral health providers.

Connecticut’s policy leaders should find these issues, that are not new, to be most disconcerting. The continuing and now heightening trend of private providers leaving insurance panels and just accepting private pay clients has significant implications as to health equity. We are reaching a point (and some will argue we are already there) where those consumers who can afford to pay out-of-pocket for mental health care will have full access to needed care. However, for most state residents who must rely on their insurance finding appropriate care is becoming most difficult.

NASW/CT calls on policy makers, health care advocates and insurers to take the following three steps as a start to addressing the issues laid out here. Reimbursement rates must be substantially increased; statutory action is need in the 2025 legislative session to limit retroactive denial of claims to 12 months look back; and insurers must dramatically improve communications and responsiveness to providers by enhancements to their provider relations staffing so that wait times are short and issues of concern are resolved in a timely fashion.

Stephen Wanczyk-Karp is the Executive Director of the National Association of Social Workers, CT Chapter.